Pac-Man Meets the Debt Collector

AI pulls the pin on a $2.5 trillion grenade

Private equity went all Pac-Man on SaaS.

From 2021 to 2025, hundreds of LBOs were underwritten on one core assumption: seat-based recurring revenue lasts forever.

AI is hitting that assumption from both sides:

Fewer employees = fewer seats.

AI coded applications = price pressure.

Volume and price. At the same time.

That’s fine. Private Equity takes the hit. Except.

They didn’t fund these deals with equity only.

They used private credit too.

Private credit comes with covenants.

Revenue floors.

EBITDA minimums.

Leverage caps.

Trip them and lenders take control. Restructuring follows. And forced markdowns follow that.

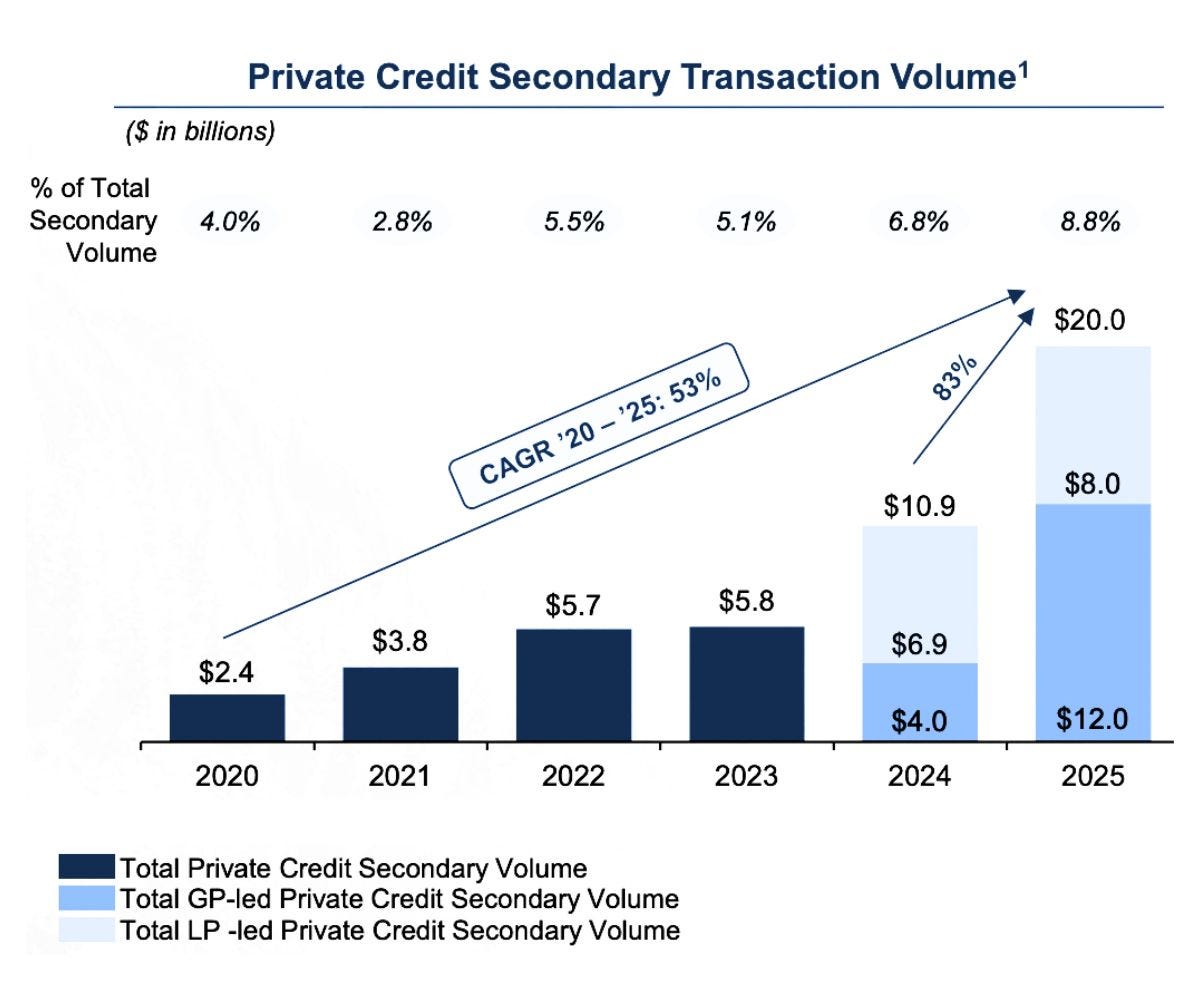

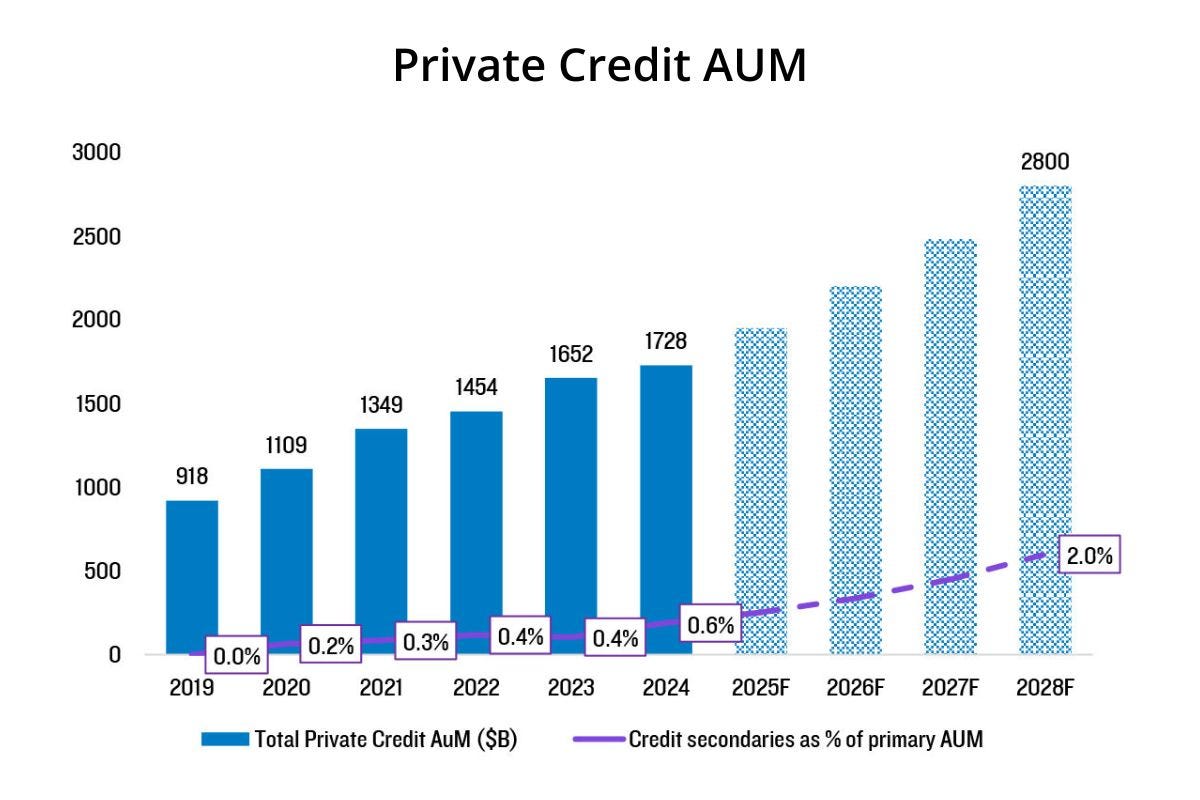

Citrini Research was first to call it: a potential SaaS extinction event is heading for the $2.5 trillion private credit market in 2026.

Your first reaction: who cares? Private funds blow up all the time.

But private credit loans are held by traditional banks and insurers.

So the chain looks like this:

AI hits SaaS revenue →

Covenants breach →

Private credit funds crack →

Banks get hit →

Contagion

Public markets have discounted legacy SaaS already. They haven’t priced in what happens when the pain from the private markets travels through the credit plumbing.

So what do you watch?

Private credit secondaries are the lie detector test:

Steep discounts (10–20% book value) → something to see here.

Near book value → nothing to see here.